June 1, 2020 – Solganick & Co. was named a top lower middle market software M&A advisor by Axial. Solganick was ranked number 2 for sell-side software investment bankers on Axial’s latest ranking.

See the full article by Axial here: https://www.axial.net/forum/the-top-50-lower-middle-market-software-firms/#The_Axial_Top_50_Software_Members

Software entrepreneurs have a plethora of options in the lower middle market capital arena, including strategic buyers, private equity firms, family offices, independent sponsors, high-net-worth individuals, venture debt providers, and search funds. Axial researched and reported overview of what the three top buyer types — strategies, PE, and family offices — tend to gravitate towards. Aaron Solganick commented to Axial that “large companies are also increasingly dipping their toes in the lower middle market. In fintech, for example, “large players like Fidelity National Financial and Finastra are definitely coming downmarket for both acquisitions and investments,” says Solganick. “Sky-high multiples — as much as 12x to 15x EBITDA — have been the norm for strategics across software industry sectors, until recently.”

“Financial investors are stepping up and becoming a lot more competitive with strategic buyers,” says Solganick. “Because there’s so much capital that has been raised by private equity firms, they’re bidding higher prices to win deals. The current Covid-19 environment has also curbed strategics from acquiring companies as they conserve their cash and implement cost controls. Financial investors as a result are scooping up companies that normally strategics would typically win.”

Rank Sector Percent of Buyer Mandates

| Rank | Sector | Percent of Buyer Mandates |

|---|---|---|

| 1 | Healthcare Technology | 9.75% |

| 2 | Financial Technology | 8.40% |

| 3 | Marketing Technology | 7.04% |

| 4 | Education Technology | 6.77% |

| 5 | Infrastructure Software | 6.51% |

| 6 | BI & Analytics | 5.69% |

| 7 | BPO Technology | 4.60% |

| 8 | ERP Software | 4.06% |

| 9 | Industrial Technology | 3.93% |

| 10 | B2B Online Marketplaces | 3.79% |

Vertical B2B Software Dominates the Lower Middle Market

Three of the top four sub-sectors, according to buyer demand, are vertical software business categories: healthcare technology, financial technology, and education technology. We examined why these areas in particular are most in demand and what top dealmakers are seeing in the space.

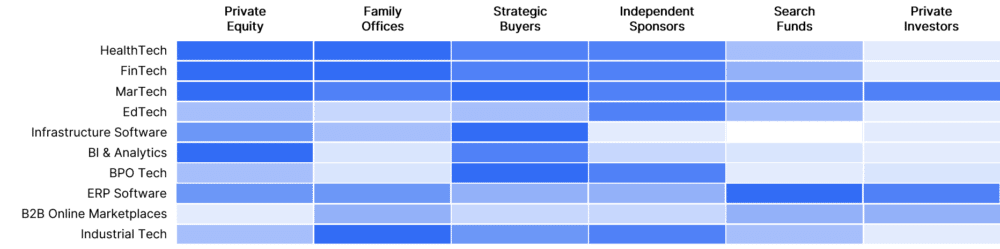

Technology demand heatmap by firm type and sub-sector

Substantial Growth of Enterprise Spending on Vertical Software

Investors’ interest in these three verticals can in part be attributed to the market size and growing demand within each respective market. Healthcare, financial services, and education organizations are expected to be some of the biggest investors in enterprise IT over the next five years. The global healthcare IT market size was valued at $125 billion in 2015, and is expected to reach $297 billion by 2022, with a CAGR of 13.2%, according to Valuates Reports. The global fintech market was valued at about $127.66 billion in 2018, and is expected to grow to $309.98 billion at an annual growth rate of 24.8% through 2022, according to the Business Research Company. Meanwhile, the global edtech market is expected to reach $277B+ by 2022, with a CAGR of more than 15% over the next five years, according to Solganick & Co.

The coronavirus pandemic will likely impact these predictions – but not necessarily negatively. According to a recent Reuters report, “many companies actually intend to accelerate [tech] spending to support thousands of employees that now have to work from home as the majority of governments around the world order national lockdowns.”

A Cash Flow Crunch for Growing Startups

IT spending has been rampant in healthcare, finance, and education alike in recent years, in large part because long-time players in these industries have been slow to adopt technology and are now investing heavily to catch up. While this presents a substantial opportunity for smaller software companies to sell lucrative subscriptions, it also means they are subject to bureaucratic approval processes. The snail’s pace at which many of these larger companies evaluate and purchase subscriptions to new technologies can put growing software businesses — many of which generated the lion’s share of their first few years of revenue from nimble startups & fast-moving early adopters — in a significant cash flow bind.

These enterprise clients may take months or even years to convert to customers. “Financial services, healthcare, and education systems are all notably slow,” says Aaron Solganick, CEO of investment bank Solganick & Co. “So, verticalized technology companies often get stuck in a no-man’s land where they have a lot of sales contracts that could potentially pan out, but they also need to stay afloat while those contracts are being negotiated.”

3 Stages of Software Companies in the Lower Middle Market

There are certainly some software companies that enjoy rapid or hyper-growth, defined by the World Economic Forum as having 20-40% CAGR or 40%+ CAGR, respectively. The majority of these companies will raise upwards of five or six rounds of growth capital until seeking a sale or an IPO. For the majority of lower middle market investors acquirers, however, these companies are almost certainly outside their purview. Instead, lower middle market players will likely look at companies in one of the following three stages of growth:

Stage 1: A Good Product, Not Yet a Business

Companies that have good technology, but have struggled to build a business around it and are now looking to sell. They may have already raised a series A or B round, so there can be several million dollars invested in the technology, but all forms of debt or minority equity financing are not available given the lack of business model viability.

Stage 2: The Cash Flow Crunch

Companies that are beyond early stage — either having raised a Series A or B, or been bootstrapped and don’t have growth potential to raise venture capital — and have developed a solid product with flat growth or bleeding cash flows. Given mistakes in initial operating investments or the capital intensity of such businesses, they require a restructuring, change of control transaction, or flexible capital infusion to overcome the cash flow crunch. Any forms of financing with aggressive return expectations are not realistic options.

Stage 3: Steady Growth

Growth stage or mature companies that have modest to substantial growth potential, but are not in hyper-growth. This group comprises “solid” businesses with mature and understandable unit economics, often run by either an aging baby boomer with no clear successor, or a couple of founders looking to find a strategic growth partner and take some chips off the table by selling a significant equity stake.

Stage 3 is where competition is most intense among middle market and lower middle market acquirers. These businesses are financeable, have mature unit economics, and have growth profiles that render them no longer attractive for VC or other forms of high growth capital.

About Solganick & Co.

Formed in 2009 by experienced investment banking professionals, Solganick & Co. is a data-driven independent investment bank and mergers and acquisitions (M&A) advisory firm that provides specialized industry-focused expertise within the Software and Tech-Enabled Services industry sectors.

Solganick & Co. offers strategic and financial advisory and relationships within the industry, a deep knowledge within these sectors, and a premium team of experienced investment banking professionals. Our team assists companies and owners in completing mergers, sales, divestitures, spin-offs and acquisitions that are strategically and/or financially beneficial to your firm’s business model and transaction goals. We also perform valuations and provide corporate finance advisory services to our clients.

As a technology-focused investment banking firm, Solganick & Co. offers an in-depth understanding of each industry sector including macro and micro drivers that lead to a successful transaction. A high closing rate with industry-focused M&A transactions gives Solganick’s expert investment bankers an accurate depiction of current M&A trends and the present deal-making climate. We provide mergers and acquisitions (M&A) advisory services to majority shareholders, CEO’s, company founders, board of directors, private equity, and family offices.

For more information, please contact us or go to solganick.com